US Solar ITC Deadline July 4 2026: EPC Action Guide

Updated (23 July): This guide originally covered the run-up to the July 4, 2026 beginning-of-construction deadline, which has now passed. Sections below have been updated to reflect what happens next for projects that met the deadline and those that didn't. The litigation status of the restored 5% Cost Safe Harbor (Oregon Environmental Council v. IRS) has not been confirmed past mid-June 2026 as of this update; verify current status before advising clients who relied on it.

The OBBBA Changed Everything: What the Law Actually Says

The Inflation Reduction Act of 2022 extended the 30% commercial solar ITC through 2032 with a planned gradual phase-down. The OBBBA, signed exactly one year ago today, altered that timeline aggressively for solar and wind. The mechanism: projects whose construction begins after July 4, 2026 must be placed in service by December 31, 2027 to qualify for any ITC. That is an 18-month window from the new-construction deadline to full operation. For most commercial solar projects in the United States, with normal permitting, interconnection, and construction timelines, 18 months from a standing start is not achievable.

The exception is the critical lever: projects that can demonstrate construction began on or before July 4, 2026 are not subject to the December 2027 placed-in-service deadline. Instead, under the IRS continuity safe harbor, those projects have until December 31, 2030, four full calendar years from the year construction began, to be placed in service and still qualify for the full 30% ITC plus applicable bonus adders.

That decision point has now passed. Every project in an EPC's pipeline falls into one of two positions as a result: those that established beginning of construction on or before July 4, 2026 now have until roughly December 31, 2030 to be placed in service. Those that didn't are on the tighter December 31, 2027 clock, or have no federal credit path at all if that date isn't realistic.

Path 1: Begin Construction by July 4, 2026

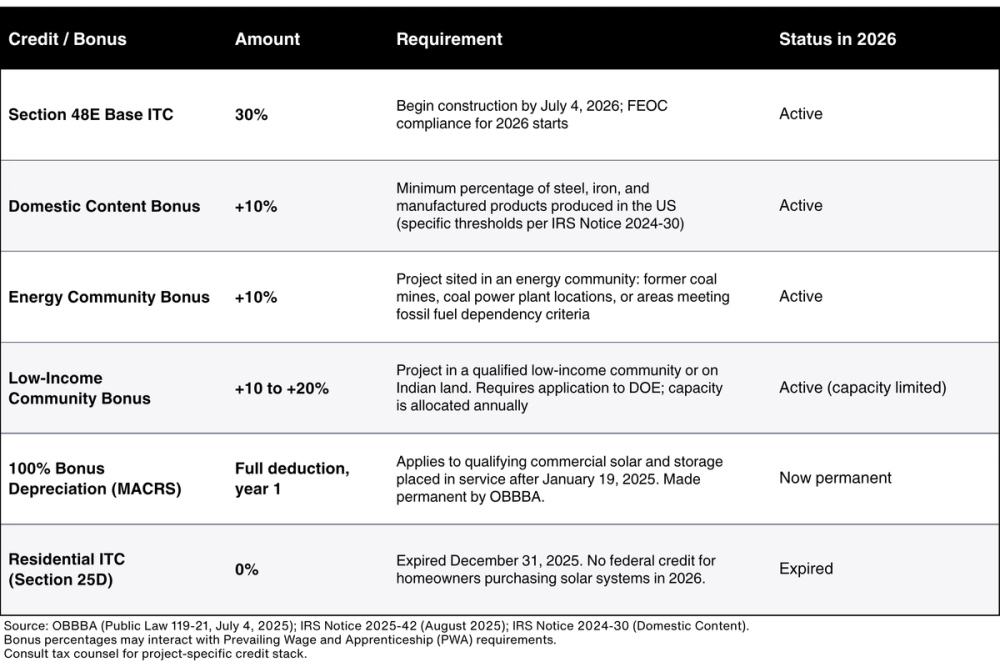

- Full 30% ITC retained (Section 48E)

- Four years to complete: place in service by December 31, 2030

- Bonus adders available: domestic content, energy community, low-income

- 100% bonus depreciation available in year one

- FEOC compliance required for construction starting in 2026

Path 2: Miss the July 4 Deadline

- Must be fully placed in service by December 31, 2027 to qualify for any ITC

- 18-month window from deadline to completion, tight for most commercial projects

- Typical permitting alone takes 3 to 6 months in most states

- Typical interconnection queue adds 6 to 18 months

- Miss both deadlines: zero federal ITC, no exceptions

The Rule Most EPCs Have Not Read: The 5% Safe Harbor Is Gone for Large Projects

Under the IRA rules that governed commercial solar through 2024, the most common way to establish "beginning of construction" was the 5% Cost Safe Harbor: pay or incur at least 5% of total project costs before the relevant date, and construction is deemed to have begun. IRS Notice 2025-42 (August 2025) eliminated that method for large solar above 1.5 MW. However, on June 6, 2026, the U.S. District Court for the District of Columbia vacated Notice 2025-42 in full in Oregon Environmental Council v. IRS, finding the IRS acted arbitrarily in eliminating the safe harbor. The 5% safe harbor is technically restored, but the legal position is not settled.

IRS Notice 2025-42, issued August 15, 2025, had eliminated the 5% Cost Safe Harbor for solar facilities with a maximum net output exceeding 1.5 MW. A federal court vacated that notice on June 6, 2026 in Oregon Environmental Council v. IRS, technically restoring the 5% safe harbor ahead of the July 4 deadline. **We have not been able to confirm what happened between that ruling and the July 4 deadline**, whether the government sought or obtained a stay, whether an appeal was filed, or whether the IRS issued new guidance on remand. Any project that established beginning of construction using the restored 5% safe harbor during that window should have this confirmed by tax counsel now, since a stay or reversal could have retroactive effect on that determination.

What the Physical Work Test actually requires

The Physical Work Test requires physical work of a significant nature to have occurred on or before July 4, 2026. The IRS Notice and established case law are specific about what qualifies and what does not.

Work that qualifies includes: excavation and site grading; installation of foundation pads or concrete footings for racking structures; physical installation of racking or mounting systems; manufacture of customised components specifically fabricated for the project; and installation of electrical conduit or cabling runs.

Work that does not qualify: preparing project plans, designs, or engineering drawings; applying for or receiving permits; ordering equipment or signing procurement contracts; conducting environmental or structural surveys; and any preliminary activity that does not physically alter the site or produce a project-specific manufactured component.

The 5% Safe Harbor remains for small systems

Following the June 6 court ruling, the 5% Cost Safe Harbor is technically available for both large projects (above 1.5 MW) and small projects (1.5 MW or less). For small projects this is relatively low-risk given the safe harbor was never eliminated for them. For large projects, the restored safe harbor carries significant legal uncertainty: the government is expected to appeal, a stay is possible before July 4, and a reversal could be retroactive. Any large project relying on the 5% safe harbor rather than the Physical Work Test should do so with full awareness of this risk and with tax counsel confirmation. The system must still be placed in service within the continuity safe harbor period. Confirm with tax counsel that the specific project configuration falls within the 1.5 MW threshold before relying on the 5% method.

FEOC: The Procurement Constraint That Took Effect January 1, 2026

Separate from the construction-start deadline, the OBBBA introduced Foreign Entity of Concern (FEOC) rules that affect ITC eligibility for any commercial solar project beginning construction from January 1, 2026 onward. FEOC refers to entities that are owned, controlled, or significantly financed by the governments of China, Russia, Iran, or North Korea, defined as entities where those governments hold 15% or more of debt or equity.

The operative rule is the Material Assistance Cost Ratio (MACR). In 2026, at least 40% of a project's relevant equipment costs must come from non-FEOC sources. This threshold rises by 5% annually. A project that fails the MACR test does not qualify for the Section 48E ITC regardless of when construction begins.

What this means for panel procurement

Most Chinese solar manufacturers, including Jinko Solar, LONGi, Trina Solar, Canadian Solar, and BYD, are considered FEOC sources. Panels manufactured in Vietnam, Malaysia, or Thailand by Chinese-owned entities are also captured by the FEOC rules. United States assembly does not cure FEOC status: a system assembled in Georgia using Chinese-origin cells remains subject to the full FEOC cost ratio calculation for those cells.

FEOC-compliant panel manufacturers confirmed as of June 2026 include: First Solar (Perrysburg, Ohio, full US supply chain), QCells/Hanwha (Dalton, Georgia), Silfab Solar (Canadian/US manufacturing), and Mission Solar (San Antonio, Texas). According to NuWatt's verified manufacturer database and PowerFlex's procurement guide, lead times for these panels have extended to 8 to 12 weeks in many markets as the July 4 deadline approaches. For EPCs who need to place orders to meet the Physical Work Test timeline, procurement decisions must be made now.

The 10-year recapture risk EPCs must explain to clients: Under the OBBBA, if a project owner claims the Section 48E ITC and then makes payments under a contract that gives a Specified Foreign Entity effective control over the project within the following 10 years, the full ITC amount must be repaid. FEOC compliance is not a one-time procurement check at installation. It is a decade-long obligation that extends through operations, maintenance, and warranty arrangements. Tax counsel should review all ongoing service contracts for FEOC exposure before ITC is claimed.

The Complete Bonus Stack: What Commercial EPCs Can Still Capture

The base 30% Section 48E ITC is the floor. Three additive bonus credits can stack on top for qualifying projects beginning construction by July 4, 2026.

Battery Storage: A Better Position Than Solar Under the OBBBA

While solar and wind face the aggressive July 4, 2026 construction deadline, standalone battery energy storage systems are in a materially better position under the OBBBA. Battery storage projects retain ITC eligibility under Section 48E through 2033. The OBBBA did not apply the same accelerated phase-out to storage that it applied to solar and wind.

Battery storage is also subject to FEOC rules for projects beginning construction from 2026 onward, but the MACR thresholds apply differently to storage components than to solar modules. Projects that began construction before the end of 2025 avoid the FEOC material assistance test entirely for battery storage.

For EPCs advising clients on combined solar and battery projects: the storage component of a solar-plus-storage system retains more favourable ITC terms than the solar component. The financial model for a combined system in 2026 should present solar and storage ITC eligibility separately, with storage's longer runway clearly communicated as a distinct advantage.

What EPCs Must Do Now That the Deadline Has Passed

Step 1: Triage the pipeline by project size

Separate every project in the pipeline into two categories based on what was actually established by July 4: projects with documented beginning of construction (via Physical Work Test evidence, or via the 5% Cost Safe Harbor if that path's legal status is confirmed current for the relevant window), and projects without it. For the second group, immediately assess whether December 31, 2027 placement in service is realistic given permitting and interconnection timelines already in progress; if not, the client needs to know now that the federal credit is likely unavailable, not discover it during tax filing. The 5% safe harbor is technically available again but legally uncertain. Consult tax counsel before relying on it. Projects that cannot begin any qualifying construction activity by July 4 face the December 2027 placed-in-service deadline and need a realistic assessment of whether that timeline is achievable.

Step 2: Verify FEOC compliance before ordering panels

Before placing any panel order for a 2026 project, confirm the manufacturer's FEOC status. Use manufacturer-issued compliance certifications (permitted under February 2026 interim guidance, IRS Notice 2026-15) as the documentation basis. Do not rely on the country of assembly alone. Confirm the origin of the cells, wafers, and key upstream components. For projects where FEOC-compliant panels are not yet secured, contact First Solar, QCells, Silfab, or Mission Solar immediately. Lead times for FEOC-compliant panels were running 8 to 12 weeks as of mid-2026; confirm current lead times directly with the manufacturer, since this figure will have moved.

Step 3: Document construction start with IRS-compliant evidence

The Physical Work Test is only as strong as the documentation behind it. For each project that will rely on the test, prepare a contemporaneous record of the physical work performed on or before July 4: dated photographs, equipment mobilisation logs, contractor sign-in sheets, and a written description of the physical work performed. The IRS specifically flags that it will scrutinise "artificial acceleration or manipulation of eligibility", the work must be genuine and of a significant nature, not a token ground-breaking ceremony. Consult tax counsel to ensure the specific activities meet the IRS standard before treating the test as satisfied.

Step 4: Update every client proposal to reflect 2026 reality

Any commercial solar proposal currently in circulation that was prepared before the OBBBA changes were fully understood needs to be reviewed against the current rules. Specifically: residential ITC proposals are now incorrect (the credit no longer exists for homeowner-purchased systems); commercial proposals must reflect the July 4 deadline clearly; any proposal citing a Chinese panel manufacturer needs to address FEOC and the MACR calculation; and any proposal or closed project that relied on the 5% safe harbor for a system above 1.5 MW during the window between the June 6 ruling and July 4 needs its beginning-of-construction determination reconfirmed against the current, resolved litigation status before that determination is treated as final. Reslink's solar proposal workflow allows EPCs to generate updated financial models with current ITC percentages, bonus stacks, and 100% bonus depreciation applied automatically from the system design, so every proposal reflects what clients will actually receive.

Frequently Asked Questions

Q1. What is the commercial solar ITC deadline in 2026?

The critical deadline was July 4, 2026, and it has now passed. Under the One Big Beautiful Bill Act (OBBBA, Public Law 119-21), commercial solar projects under Section 48E needed to begin construction on or before that date to retain the standard completion window. Projects beginning construction by that date have until December 31, 2030 under the IRS continuity safe harbor (four calendar years from the year construction began) to be placed in service and claim the full 30% ITC. Projects that do not begin construction by July 4 must be fully placed in service by December 31, 2027 to qualify for any ITC. Projects missing both dates receive no federal Section 48E investment tax credit. The residential solar tax credit (Section 25D) is separately gone: it expired December 31, 2025 with no replacement for homeowners who purchase systems directly.

Q2. Does ordering solar panels before July 4 count as beginning construction?

On June 6, 2026, a federal court vacated IRS Notice 2025-42 in full, technically restoring the 5% safe harbor for large solar projects above 1.5 MW, with the appellate timeline expected to run past July 4. We have not confirmed the outcome of that appeal or any stay motion as of this update; any project that relied on the restored safe harbor between June 6 and July 4 should have that determination reconfirmed with tax counsel now that the litigation may have progressed. A reversal could have retroactive effect on projects that relied on the restored safe harbor. For projects of 1.5 MW or less, the 5% safe harbor was never eliminated and remains available with low legal risk. For projects above 1.5 MW, the Physical Work Test, excavation, foundation installation, racking installation, or manufacture of custom project-specific components, remains the most legally durable path given the appeal uncertainty. Consult tax counsel before relying on the restored 5% safe harbor for any project above 1.5 MW.

Q3. What are FEOC rules and which solar panels are affected?

FEOC stands for Foreign Entity of Concern. Under the OBBBA, projects beginning construction from January 1, 2026 must meet the Material Assistance Cost Ratio (MACR): in 2026, at least 40% of relevant equipment costs must come from non-FEOC sources. FEOC entities are those with 15% or more ownership or financing from the governments of China, Russia, Iran, or North Korea. Most major Chinese solar manufacturers, including Jinko Solar, LONGi, Trina Solar, Canadian Solar, and BYD, are FEOC sources. US assembly does not cure FEOC status if the cells are Chinese-origin. FEOC-compliant manufacturers include First Solar (Ohio), QCells/Hanwha (Georgia), Silfab Solar (Canada/US), and Mission Solar (Texas). Manufacturers may issue self-certification letters confirming FEOC compliance under interim IRS guidance (Notice 2026-15, February 2026). Consult tax counsel to verify FEOC compliance for your specific supply chain before claiming the ITC.

Q4. Is the residential solar tax credit still available in 2026?

No. The Residential Clean Energy Credit (Section 25D), which provided a 30% federal tax credit to homeowners who purchased and installed solar systems, expired December 31, 2025 under the OBBBA. There is no federal ITC for homeowners who purchase solar systems directly in 2026. There is no replacement credit and no phase-down: the credit value went from 30% to 0% on January 1, 2026. Homeowners who use third-party financing, specifically solar leases or power purchase agreements (PPAs), may still indirectly benefit from the commercial ITC because the financing company, which owns the system, claims the Section 48E credit and typically passes a portion of the value through lower monthly payments. The financing company must begin construction by July 4, 2026 for this to apply.

Q5. Does 100% bonus depreciation still apply to commercial solar in 2026?

Yes. The OBBBA made 100% bonus depreciation permanent for qualifying commercial energy systems, including solar panels, solar plus battery storage, and standalone battery storage systems, placed in service after January 19, 2025. Under MACRS, businesses can deduct the full cost of a qualifying solar system in the first year it is placed in service, regardless of the system's expected useful life. This is separate from the Section 48E ITC and applies independently of whether the project meets the July 4 construction start deadline. Combined with the 30% ITC, the tax benefits from the credit and first-year depreciation can offset 50 to 60% or more of total project costs in year one for qualifying commercial projects. Consult a tax advisor to model the specific interaction of ITC and bonus depreciation for your project, as ITC basis reduction rules affect the depreciation calculation.

Q6. How does the July 4, 2026 deadline affect battery storage projects?

Battery energy storage systems have a significantly better position than solar under the OBBBA. Standalone battery storage retains ITC eligibility under Section 48E through 2033, without the accelerated construction-start deadline applied to solar and wind. Battery storage projects beginning construction in 2026 are subject to FEOC rules, but the MACR thresholds apply differently to storage components than to solar modules, and storage projects that began construction before the end of 2025 avoid the FEOC material assistance test entirely. For commercial EPCs advising clients on combined solar and battery projects in 2026, the solar component faces the July 4 deadline while the storage component retains flexibility through 2033. These two components should be modelled separately in any client proposal that includes both solar generation and battery storage.

You May Also Like

- Brazil Solar Curtailment 2026: What EPCs Must Know Before Their Next Project

- Japan FIP Auction 2026: September 30 Deadline Guide for EPCs

- Intersolar Europe 2026: Munich Guide for Solar EPCs

Sources

- One Big Beautiful Bill Act (OBBBA), Primary Law — Public Law 119-21 — Signed July 4, 2025. Sections 70512 and 70513: construction start deadline July 4, 2026 for Section 45Y and 48E credits; placed-in-service deadline December 31, 2027 for projects missing the construction start deadline; residential ITC (Section 25D) expired December 31, 2025.

- IRS Notice 2025-42 (Primary), August 15, 2025 — irs.gov — Eliminates 5% Cost Safe Harbor for solar facilities above 1.5 MW net output; Physical Work Test is sole method for large solar; continuity requirement: placed in service within 4 calendar years of construction start.

- IRS Notice 2026-15 (Primary), February 2026 — Interim FEOC compliance guidance: manufacturer self-certification letters accepted as documentation for FEOC compliance; Material Assistance Cost Ratio (MACR) clarifications.

- KPMG OBBBA Tax Credit Analysis — kpmg.com — Physical Work Test requirements: excavation, installation of key components required; preliminary activities (planning, permitting) excluded; confirms 5% Safe Harbor excluded for wind and solar above 1.5 MW.

- Mayer Brown Legal Analysis, August 2025 — mayerbrown.com — Construction start deadline for Sections 45Y/48E: before July 5, 2026; OBBBA enacted July 4, 2025; guidance addresses strict enforcement preventing circumvention.

- Greenbaum Law OBBBA Safe Harbor Guide, October 2025 — greenbaumlaw.com — Beginning construction by July 4 is not sufficient alone; continuity requirement mandates ongoing progress; Continuity Safe Harbor: placed in service within 4 calendar years.

- PowerFlex FEOC Guide, March 2026 — powerflex.com — MACR threshold 2026: minimum 40% non-FEOC equipment; rises 5% annually; February 2026 interim guidance allows manufacturer certifications; FEOC = 15%+ ownership by China/Russia/Iran/North Korea.

- NuWatt FEOC Solar Deadline Guide, February 2026 — nuwattenergy.com — FEOC-compliant manufacturers: First Solar (Ohio), QCells/Hanwha (Georgia), Silfab (Canada/US), Mission Solar (Texas); lead times 8-12 weeks as deadline approaches.

- SEIA Solar Market Insight Report, Q3 2025 — seia.org — 90 GW of projects well-positioned to safe harbor or begin construction before July 4, 2026; commercial and community solar developers expected to begin physical work on projects.

- Litigation status note: Sources cited above for the Oregon Environmental Council v. IRS ruling are dated June 6-17, 2026. We could not locate a source confirming the case's status (stay, appeal outcome, or IRS remand response) as of this update. Verify current docket status before publishing.

Related Articles

Solar Tax Credit Deadline 2026: EPC ITC Guide

Learn how U.S. solar EPCs can still claim the Investment Tax Credit after the July 4 2026 deadline, with eligibility rules, required documentation, financing impact, and step‑by‑step actions.

EU Hybrid Solar‑Wind Projects: An EPC‑Focused Guide

Learn how EU hybrid solar-wind projects help EPCs meet policy goals, reduce grid upgrades, and secure financing

FERC Interconnection Reform 2026: EPC Guide

PJM's interconnection timeline hit 8+ years. FERC's Order 2023 reforms are still being enforced. What's actually changing for solar EPCs.